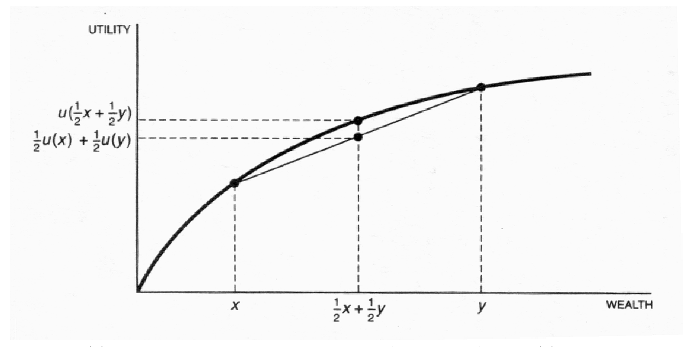

Figure —The expected utility of the gamble is 1/2U(X)+1/2U(Y). The utility of the expected value of the gamble is U(1/2X+1/2Y). In the risk averse case depicted the utility of the expected value is higher than the expected utility of the gamble. (Schneider and Kuntz-Duriseti, 2002; modified after Varian, 1992).